1) The world no longer has the head room to use gas a transitional fuel. If gas replaced all coal in electricity generation, an impossibility in of itself, the world would still have well over 2°C of average global warming.

The idea of gas as a “transition” fuel arose in the time when wind and solar energy were expensive and little used. But we have passed that point. The cost of solar has plunged 90 per cent in the past decade, wind more than 60 per cent. Exactly what role is gas supposed to serve in electricity generation in Australia?

2) Extracting gas from the Narrabri field in NSW at the mooted rate of 60 petajoules (PJ) a year is likely to require a price of at least $6 a gigajoule, and probably more like $7-$8 GJ to be economic. Imported LNG is likely to cost a bare minimum of $A7.50/GJ and no-one’s going to build an import terminal without a higher price than that. Nor do we see Narrabri as increasing price competition, mainly because its owned by Santos, and so the producer oligopoly remains in place.

3) In Australia we are already seeing batteries starting to compete directly with gas peakers. AGL has signed battery contracts on an unsubsidized basis not just in Queensland with Vena for a 100 MW/1.5 hour, battery, but also in NSW with Maoeneng for 200 MW/2 hours of big batteries. AGL is the user of the battery in both cases but the fact that there are two different capacity providers in two different NEM regions as evidence that the market economics must, at a minimum, be close in Australia.

4) One of the main engines of global gas consumption growth, the US shale gas revolution, has run right out of steam.

a) Production is flat.

b) Market prices are lower than those required to justify new investment

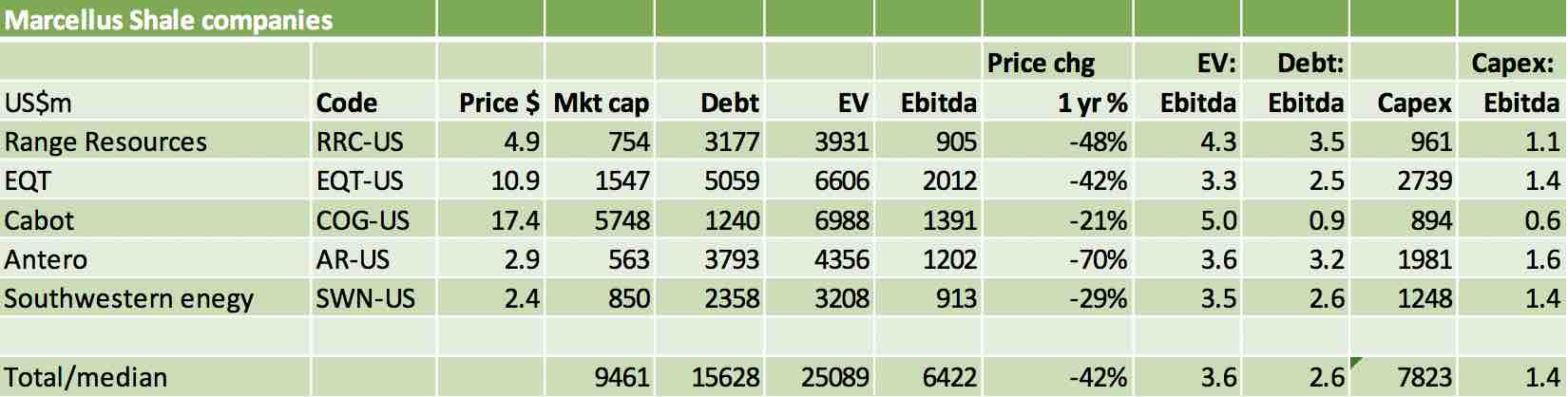

c) The Marcellus Shale gas industry is cashflow negative but growth has been funded by debt and most companies are under severe financial stress. Even so the industry wants to expand because:

The industry decline rate is about 25% per year;

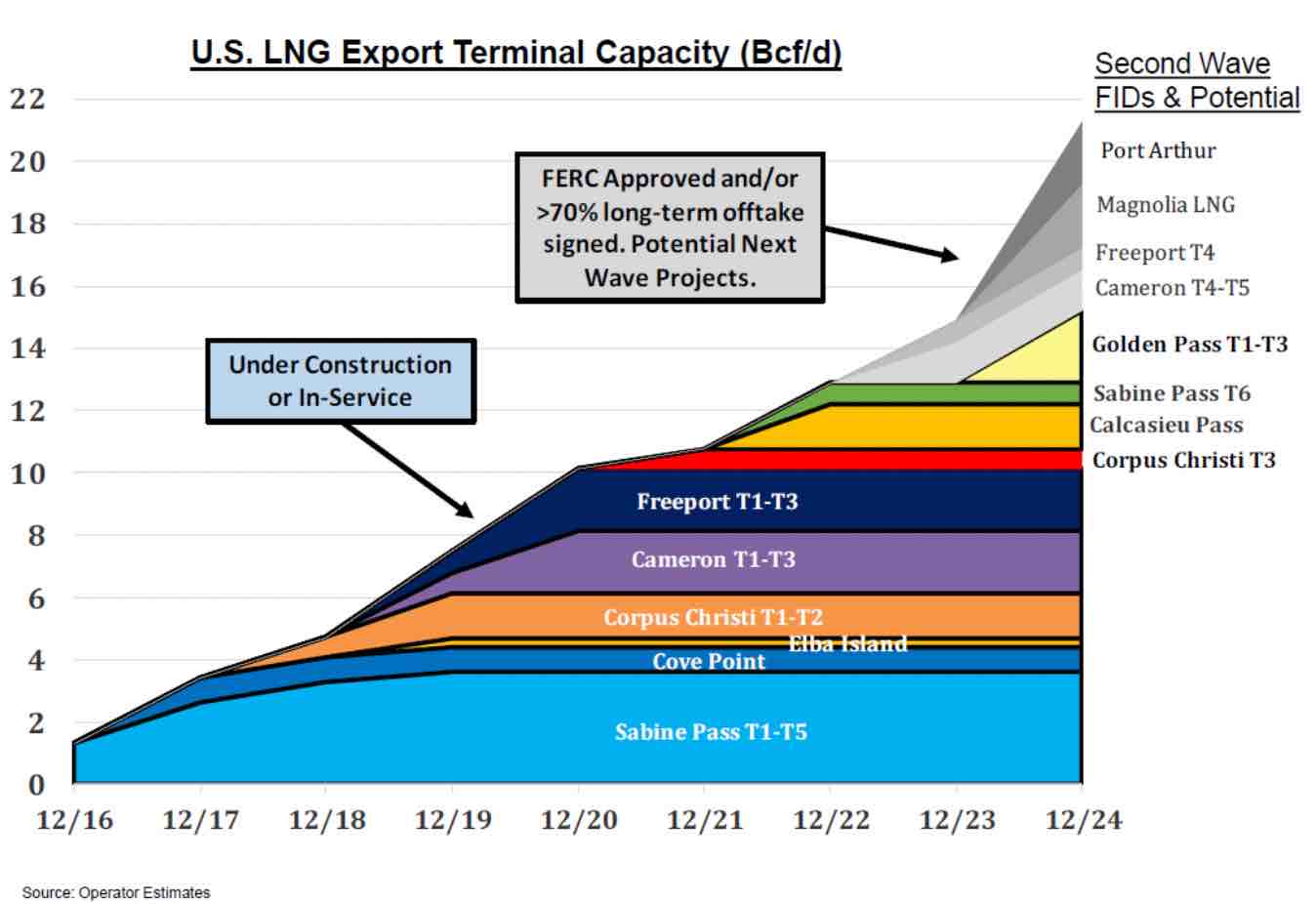

Exports of LNG from the US are hoped to grow strongly over the next few years

Gas is still replacing coal and nuclear in the US electric power industry.

d) Despite the positive volume growth story, share prices have completely collapsed for several players and the debt industry is no longer willing to finance the industry without it going cash flow positive.

e) In some parts of the industry productivity growth has stopped. That shouldn’t surprise people as when volume growth declines so it takes much longer to take advantage of the learning rate.

5) Will we see new gas power stations in NSW? AGL and EnergyAustralia both have plans to build one, but have not proceeded.

If Narrabri is developed perhaps even Sunset Power or Shell (via ERM) might build one in NSW’s proposed renewable energy zone (REZ), which happens by coincidence to be right next to Narrabri. This would avoid gas transmission costs and would have the electricity transmission paid for by the Govt.

Even so, we can’t see it making any material difference to electricity prices and expect it would be struggling to get much of a foothold in the daily balancing market.

Gas generation is an expensive proposition on almost all grounds.

Gas’ role in electricity is about 34% of a typical country

From a global perspective gas provides 23%of global electricity generation.

However, this number is downwardly biased by the low gas share in China and India. If we look at the median share of gas in a country’s generation mix it’s about 34%.

Also ,gas fuelled electricity has been growing quickly on a global basis:

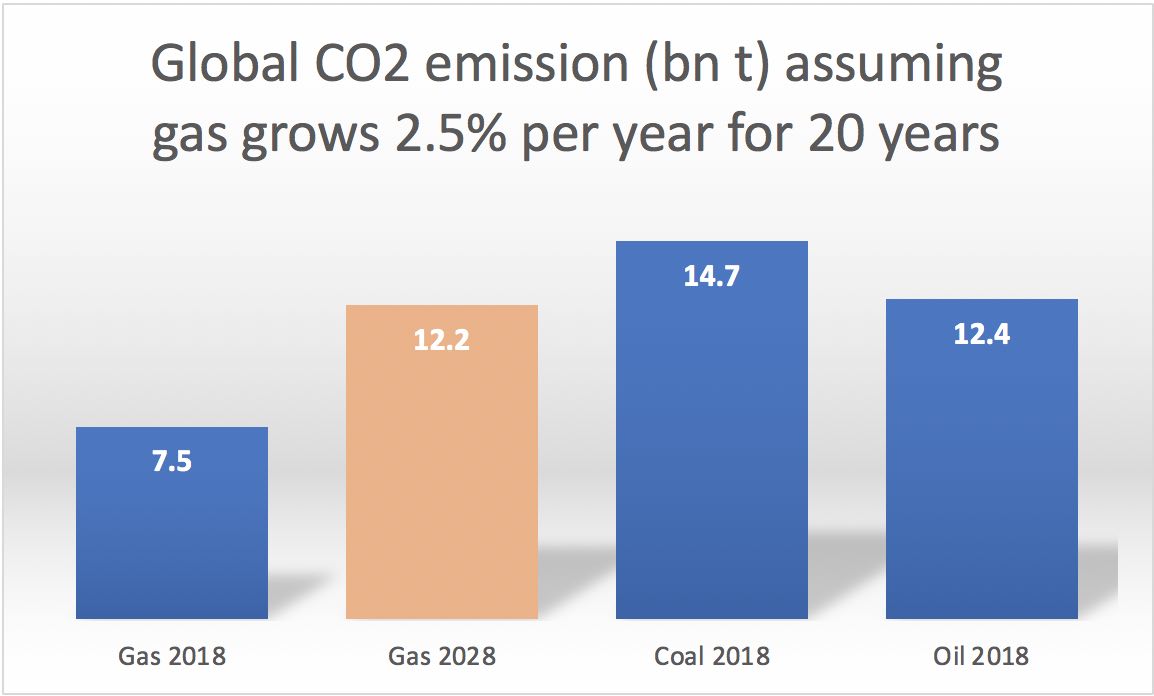

Gas Co2 Emissions are large, and growing

Gas CO2 emissions total around 7.5 billion tonnes a year, and could be on their way to 12 billion tonnes a year. They are derived from two main sources:

(1) emissions associated with gas extraction, which breaks down to fugitive gas and CO2 produced if electricity is used to run the gas compression system. This occurs in pretty much all of coal seam gas production in Queensland.

(2) CO2 emissions when the gas is burned primarily for electricity production.

First, let’s again look globally. Gas emissions have grown 2.5% a year (compound) from 2000-2018 (2.1% from 2010).

Assuming 2.5% growth from 2018 to 2038 ,they will be on par with coal and oil emissions in 2018. In ITK’s view, that alone mitigates against gas’s role as a transition fuel.

Of course, coal emissions might reduce as a result but it’s not enough any more to avoid dangerous climate change. Not even close.

Regarding fugitive emissions the evidence is far less clear.

If we look at the Santos data presented as part of the environmental impact statement for Narrabri we would conclude that only about 0.5 -1.0 mt per year of CO2 emissions arising from production of the gas, or about 26-34 mt/co2 over a 25 year lifetime.

Most of that gas appears to be CO2 that is actually part of the CSG (i.e. you extract the methane but get some CO2 in the mix). Similarly, small to modest numbers appeared in the EIS for APLNG in QLD that I read.

ITK notes that no good work has ever been reported in Australia that enables direct measurement of fugitive emissions (gases given off in the gathering process or resulting from methane venting).

The fugitive emissions may well be higher than Santos estimates, but in our view they aren’t the main game. For what it’s worth, ITK also believes that water contamination from quality CSG production is likely to be low to non existent (concrete cased steel wells) and that salt production from CSG water treatment is very manageable.

There is no good science that supports the idea of damage to surface water from properly managed fracking. Many science reports have said so. If you live by climate science, you also support fracking science.

Cost of Narrabri gas – uncertain and variable

Corelogic, a gas consultant., estimates a cost of $6/GJ for Narrabri gas.

There are transport costs on top of that, although if you build a gas power plant near the site (see for instance the Condamine power station in Qld) the transport costs will be minimal.

The $6 GJ estimate is really not known with any confidence and ITK believes a reasonable range is $5 GJ to about $8 GJ, possibly biased to the higher end of the range.

Gas has not been produced in quantity from Narrabri (Gunnedah Basin) or indeed NSW coal fields before.

The scale of the operations will not approach those in Qld, but 60 PJ a year is not to be sneezed at.

There are two main drivers of cost of coal seam gas.

(1) Gas well flow rates, and decline rates. And

(2) the often overlooked labor rates.

One of the biggest mistakes the author has made in research in the last six years was underestimating the variability of oil drilling costs. That is the cost of drilling when oil fell from US$100/ to US$50 barrel was phenomenal.

The Schlumbergers and Haliburtons of the world cut their prices dramatically. We will get back to US gas prices shortly but the point is that costs are not fixed.

According to Santos, the Narrabri project amounts to 850 vertical and lateral wells (mostly 3 wells per pad) spaced at say 750 metres with depth to coal seams of 500 metres to 1200 metres (mostly a bit deeper than in Qld).

The Bibblewindi multilateral pilot was flowing at 1 PJ per year back in 2009 which is a good flow rate but far from enough data to draw any real conclusions. The higher the flow rate the fewer number of wells and therefore the lower capital expenditure per PJ of production.

The best information ITK can find on the reserves and well profile remains the Independent Experts Report provided at the time of the Santos takeover of Eastern Star Gas in 2010.

2P certified reserves, mostly related to the relatively thick Bohenas seam, which rather than being cleated as in Qld coals is vertically fractured, were about 1500 PJ. Much higher resources were discussed taking into account other seams.

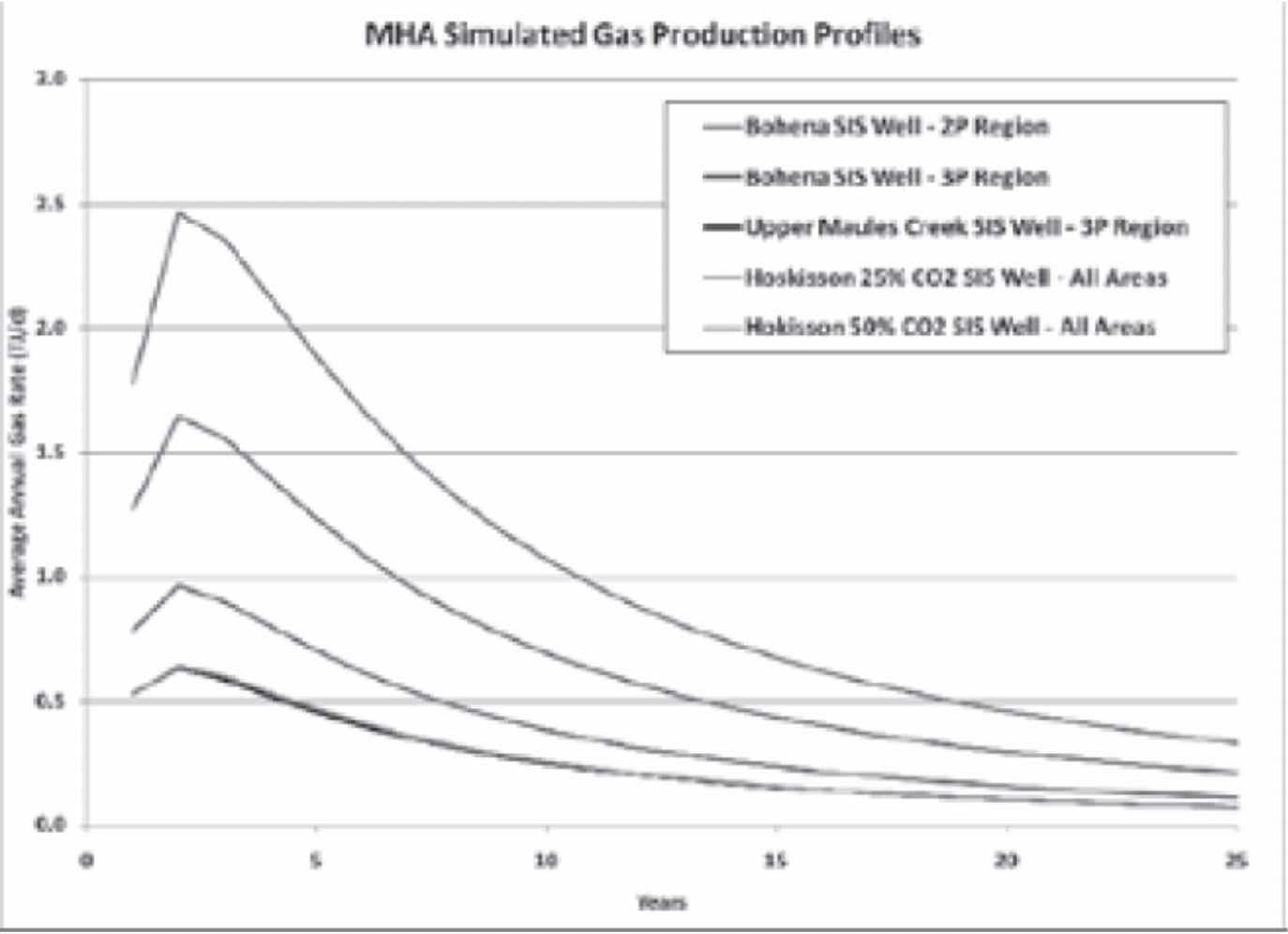

The current production plan submitted by Santos calls for 840 wells producing 200 TJ per day or around 60 PJ per year for 25 years.

Of course, production will tail off towards the end of the development but as submitted the production profile implies about 1500 PJ of production, more or less in line with the 2P Bohenas seam reserves estimate.

As the top line in the figure below shows production is expected to average about 2.25 TJ/day a year for the first five years (much higher than the average well in QLD but also more expensive to drill) and wells are still expecting to be producing 0.5 TJ day 20 years out.

Santos’s current plan of 840 wells implies about 2 PJ lifetime production per well, very different from the production profile just discussed. The point being that the information publicly available suggests a wide range of reasonable cost outcomes.

APLNG, four years into production with what is generally regarded as a high quality CSG resource in QLD has maintenance capex and opex running at around $4/GJ of annual production. Virtually all of this relates to upstream operations.

That $4 excludes the initial start up capex, in Narrabri’s case that is basically the gas processing plant, associated reverse osmosis and site development costs. There is also the significant field acquisition and subsequent exploration cost to recover coming to over $1.5 bn.

All in all there is good reason to expect $6 GJ of cost that needs to be recovered.

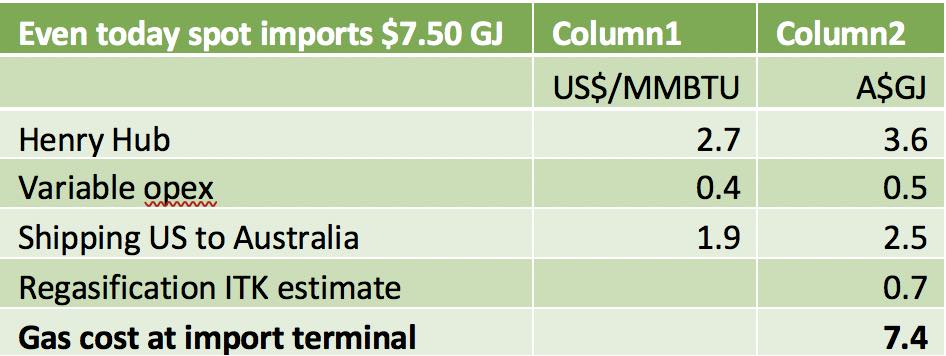

Imported gas – rough economics

If we look at Origin Energy’s 2019 investor day presentation we can see what imports of gas from the US into Australia would come to about A$7.50 GJ

Gas imported from the Northwest Shelf would be lower cost but not necessarily lower priced.

In ITK’s view Narrabri gas and imports are likely to have similar cost base but it’s a bigger commitment to build Narrabri as you then have to make it work every year for 25 years.

Gas from the Beetaloo Basin in the Northern Territory won’t ever come to NSW unless it’s an oil by-product and therefore low cost.

Looking at gas power in NSW

A quick summary of the pool performance is shown below:

Probably the most relevant comparison is Tallawarra .

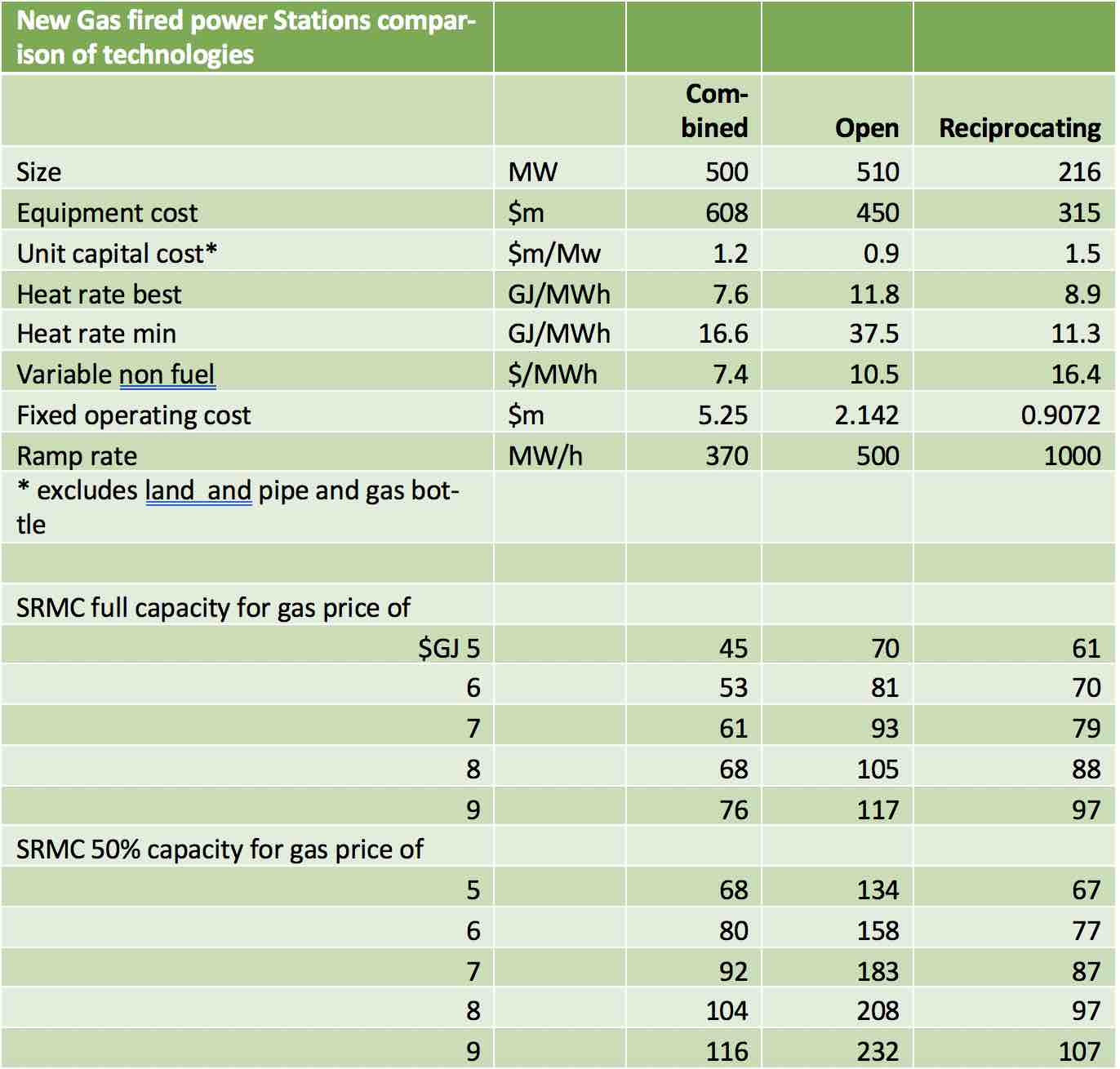

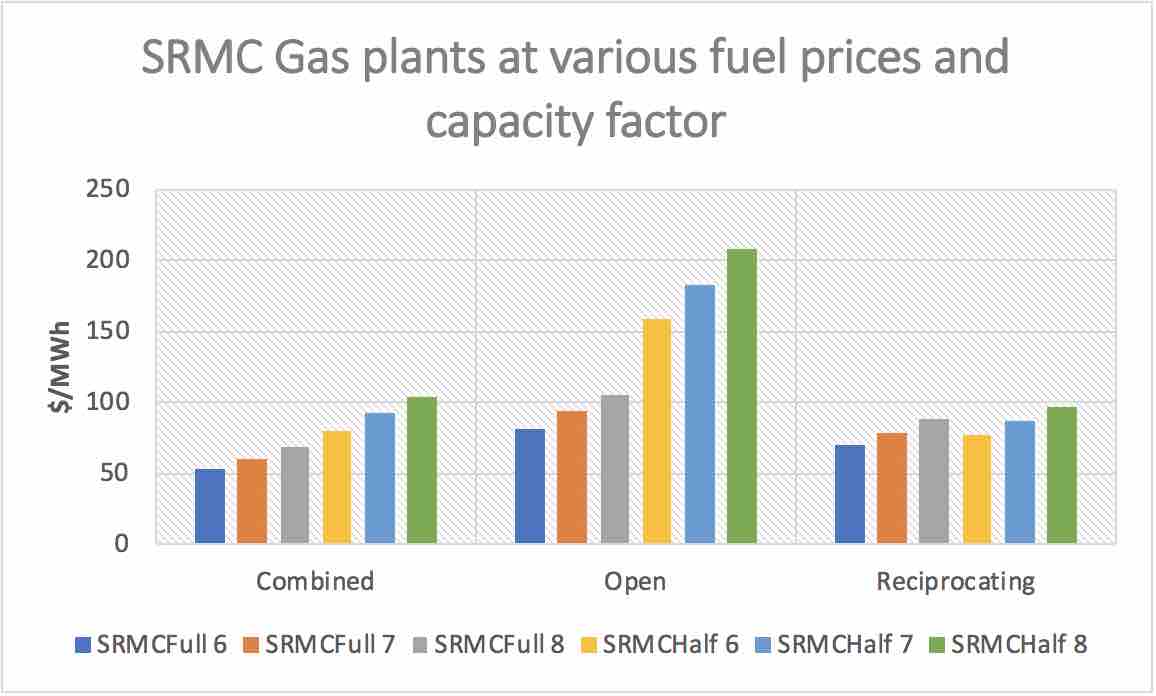

New gas generation short run marginal cost.

Next we compare a few key stats for different types of new gas power stations. GHD provided some excellent data on a report to the NSW Govt.

Note that my experience is that in reality capital costs will most likely be higher than reported here.

Obviously, you need to charge more than the short run marginal cost (SRMC) of gas to get a return on capital, but we ran out of time to do an LRMC (long run marginal cost)

Long and short at gas prices of $7 GJ or higher LRMC is going to be unattractive for energy, although it may still work for “firming.:”

US shale has moved from miracle to disaster for producers.

Heres a quote from a very recent Reuters article:

“Over the latest decade, the shale revolution turned the United States into the world’s largest crude producer and a force in energy exports. Yet the revolution did not translate to higher stock prices. The S&P 500 Energy sector only gained 6% for the decade, far less than the 180% return for the broader stock market.”

The rig count tells a story

As do the numerous recent stories of bankruptcy, writeoffs and debt.

Essentially the point is not that shale oil in the US hasn’t been a wonderful thing (from an oil production point of view) but rather that the industry has never been cash flow positive. The production growth has been powered by debt.

Now, however, the debt providers have got worried and stopped advancing new funds.

This will mean that production growth will stop, production may even decline marginally and producers will go into cash flow mode.

Haliburton, a leading oil well drilling company saw North American revenues decline 21% in Cal 19. Haliburton went on to say:

“Early indications are that our US land customers will reduce capital spending approximately 10% from 2019 levels. I believe that the current level of DUCs in the market will allow operators to spend less money on new well construction and drag more of it to completions.

Depressed gas pricing is negatively affecting the activity outlook in the gassy basins, which will likely bear the brunt of the activity reductions in 2020.”

The industry has a natural decline rate of about 25%. That is, if the entire industry stopped drilling over 12 months, production would decline 25%.

Still, just like the decline rate of individual wells the overall industry decline rate would slow over time.

I obviously can’t do analysis of even one US Shale company let alone the industry. Still here’s a summary of sorts of five Marcellus (largely gas) oriented, listed USA shale producers.

Note that these business continue to have capex higher than ebitda, never mind interest or tax costs or recovery of invested capital Ie they are still running cash flow negative. It’s the fear of going bankrupt that has continued to drive down share prices.

Replacement and demand growth makes industry reluctant to cut production

Because of the industry decline rate and because drilling high quality wells provides immediate cash flow the industry continues to produce more than can be absorbed by domestic gas.

The industry hopes that growth in LNG exports can substitute for the over supply in the domestic market.

For instance the following figure shows what Range Resources hopes will happen to US LNG exports.

Equally the industry hopes gas can continue to replace coal and nuclear in the USA for electricity generation:

The industry hopes for North American cumulative demand growth of 21 BCf/d (8333 PJ/year) over the next five years of which about 1/3 may come from oil byproduct production.

According to Range, JP Morgan estimates the dry gas industry needs a price of about $3.30/mcf (about A$5 GJ) to earn cost of capital. However, industry forecasts are for lower prices.

For instance, here are Antero Resources basically is looking for US$2.35 MMBTU (about A$3.50 GJ) suggesting that the industry still has sharp problems in front of it.

Outside of the Permian Basin there is also some evidence that productivity growth is slowing and I can’t say this is surprising.

However, every company believes it’s the only one that can keep lowering its costs and each of the companies normally believes (or tells investors) it has the best resource.

David Leitch is a regular contributor to Renew Economy. He is principal at ITK, specialising in analysis of electricity, gas and decarbonisation drawn from 33 years experience in stockbroking research & analysis for UBS, JPMorgan and predecessor firms.